About your AVCs.

Additional Voluntary Contributions (AVCs) are a way for you to make extra contributions to your pension which allow you to build up a separate pot of money that can be used to supplement your retirement income or provide additional lump sum benefits. You can't pay in any more AVCs, but you can still choose how your money is invested, subject to the level of investment risk you're willing to take.

You should read the section about investment risk to better understand how the investments might work for you and take a look at how the investment funds are performing.

The money you have contributed as AVCs to the Tesco PLC Pension Scheme will continue to be looked after by the Trustee. However, the Trustee cannot guarantee the performance of the investment funds.

You can read more about AVCs in our AVCs leaflet.

Five investment options to choose from.

1. The Standard Life Index-Linked Bond Pension Fund

This fund invests mostly in index-linked bonds, which are loans to governments that have a rate of interest agreed for the period of the loan that moves with inflation. The majority of this fund is usually invested in UK Government bonds, but also invests in overseas government bonds and corporate bonds.

The objective of the fund is to provide long term growth from a combination of income and capital growth, by investing mainly in index-linked stock issued by the UK government. This fund is actively managed.

The price of units will go up or down, depending on how the assets in the fund perform.

2. The Standard Life Managed Pension Fund

This fund is mainly invested in shares with the rest invested in other assets such as bonds, money markets, alternatives or unlisted assets. The investments in these funds can be from around the world, including emerging markets.

It is actively managed to take advantage of the investment opportunities seen by Standard Life's investment teams.

The objective of this fund is to provide long term growth by investing in a range of asset classes, sectors and geographies whilst spreading the risk across a number of different funds.

The price of units will go up or down on a daily basis, depending on how the assets in the fund perform.

3. The Standard Life BlackRock ACS 30:70 Global Equity Tracker (Hedged)*

This stock market linked fund is approximately 30% invested in the shares of UK companies, with the rest invested in overseas companies.

The objective of this fund is to provide a return on your investment through a combination of capital growth and income.

The fund is passively managed, which means that it aims to provide returns in line with the markets in which it invests. It is also 'currency hedged', meaning that it aims to overcome the long-term effects of changes in the value of the pound relative to other currencies.

The price of units will go up or down on a daily basis, depending on how the assets in the fund perform.

*managed by BlackRock

4. The Standard Life Deposit & Treasury Pension Fund

This fund was introduced on 1 June 2017 to replace the Prudential Deposit Fund. The purpose is to protect the value of your fund and provide 'cash-like' returns.

The primary aim of the fund is to maintain capital and provide returns before charges in line with short-term money market rates, by investing in deposits and short-term money market instruments.

The price of units may move up or down, so the value of your funds isn't guaranteed. Also, the charges applied to your fund may be greater than the returns in some years, which could make your fund value fall.

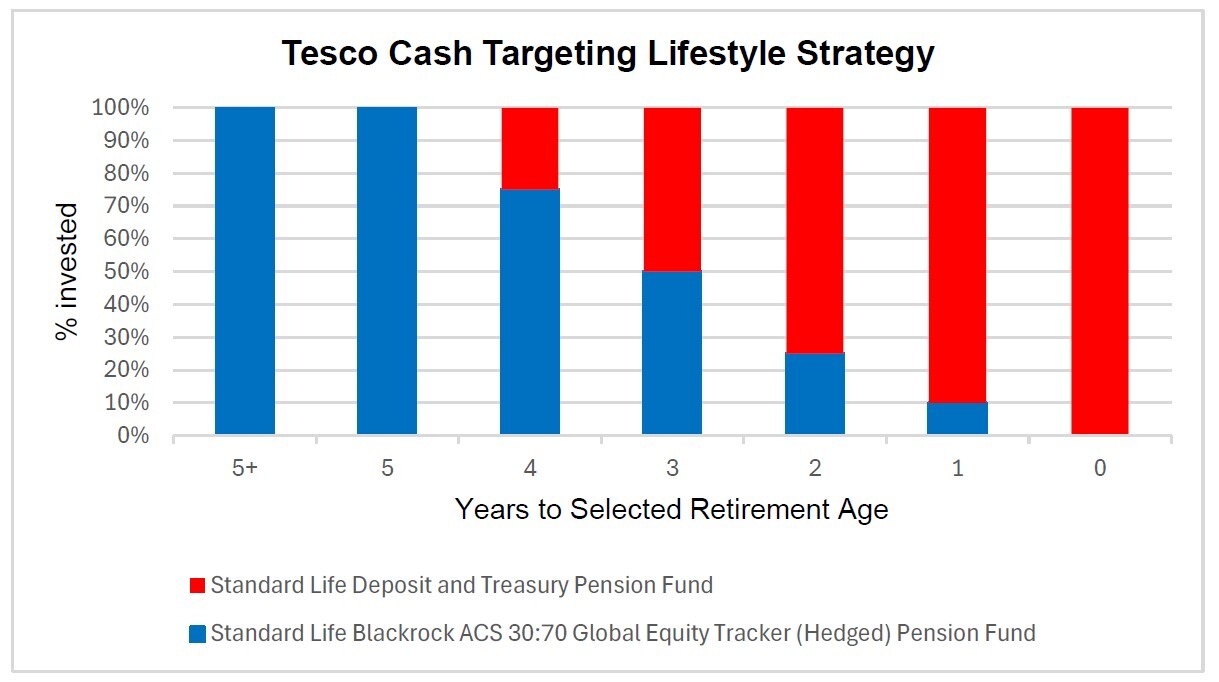

5. The Tesco Cash Targeting Lifestyle Profile

The Tesco Cash Targeting Lifestyle Profile matches the type and risk of investments to the time you have until retirement. If you're some way from retirement, it will invest in areas that give better prospects for growth over the longer term - like stock markets (the Standard Life Blackrock ACS 30:70 Global Equity Tracker (Hedged) fund – see above).

When you're five years away from the retirement age you've selected on the application form, the fund will gradually switch into the Standard Life Deposit and Treasury Fund . This is because when you retire you can take up to 25% of the value of your total Tesco pension as tax-free cash. If you wish, you can use all or part of your AVC savings as tax-free cash, subject to the Company's consent. As many retiring members have chosen to take their AVC savings as cash, the Lifestyle Profile aims to hold your savings in cash to match this requirement.

This option combines the opportunity to take advantage of growth while you're younger and have time to take the risk of changing share values, with the security of lower risk investments closer to retirement that are in line with the way that members often choose to receive their AVC savings.

Standard Life apply a charge to any monies invested in its funds. This is known as the Fund Management Charge (FMC). Additional expenses may also be deducted from some funds. These include items such as custodian fees, registrar and regulator fees. As the additional expenses relate to expenses incurred during the fund management process, they can change. The factsheets provide full information on the charges that currently apply.

Please note however, the Tesco Trustee has negotiated a discount of 0.55% per annum on the total charge that applies. This means that if a fund has a charge of 1% per annum (including additional expenses) the actual charge is 0.45% per annum.

The Prudential Deposit Fund

This fund closed on 31 May 2017 to members who don't have an investment in this fund.

This fund is very much like an interest-bearing bank or building society account. All your contributions are invested and interest is added. Once the interest is added to your fund, it can't be taken away, so the value of the fund can't go down. There are no penalties whenever you move your fund. The fund earns a variable rate of interest rate and is currently linked to the Bank of England base rate (although this can be reviewed by Prudential) .

Deposit funds are a 'low risk' type of saving. This may be more suitable for members who don't want to take any investment risk and who are closer to retirement.

For younger members who are a long way from retirement, the safer but lower returns mean your fund may not increase as fast as your earnings or inflation during your career. Over many years, the investment return on this type of fund may be lower than the long-term return on higher risk investments, like stocks and shares.

What is investment risk?

Investments can go up in value a lot, a little, or stay the same and possibly even go down. This is often due to share prices fluctuating or interest rates and inflation changing.

Investment Risk is the amount of chance you are prepared to take on money you are investing. Basically, the greater the return you want, the more risk you'll have to accept. Or, if you want to know where you stand from the start, with a less volatile return, then your investment is likely to earn less.

What might affect your decisions?

The number of years to retirement may influence your choice of investment funds because over time risk tends to even itself out. If you invest over a long period of time there is more time to recover any losses after a fall in the stock market.

How the Trustee reviews the AVCs.

Part of the job of the Trustee is to ensure the AVC investment choices are appropriate for the scheme and members. The Trustee has specialists to review the AVC investment choices, and regularly update them depending on how each fund is performing.

The 3 main objectives are:

- to provide a suitable range of investment options to satisfy most members' reasonable risk profiles

- to ensure the investment options are suitably managed to maximise the return with an acceptable level of risk

- to ensure the investment returns on the funds are in line with what the Trustee expects

Based on this advice, the Trustee can opt to remain with the current investment choices, or to switch to different providers.

Taking your AVCs.

Your AVCs can be used in the following different ways:

- As part of your tax-free cash lump sum

You can take up to 25% of the value of your total Tesco pension and AVCs as tax-free cash. If you wish, you can take all or part of your AVC fund as tax-free cash. If your fund is less than the 25% maximum allowed, you can take some tax-free cash from the pension scheme too.

- Buy a pension outside Tesco (eg, an "open market" annuity)

When we calculate how much pension your fund will buy, we divide your fund by a conversion factor. The factors may change from time-to-time to take into account, for example, the cost of buying the additional pension. Once your AVC fund has bought extra pension, it is added to your Tesco pension and treated in the same way.

- A combination of tax-free cash and extra Tesco Pension

You can have a combination of the above two (within certain limits). Please see the information above.

- Buy a pension outside Tesco or annuity

An annuity is a pension you can buy with some or all of your fund value at retirement. This is sometimes called an "open market" option. It can provide a fixed or variable amount of income for either a fixed term or for life. You can choose the type of annuity you wish to buy. Different providers will offer different features, rates of payment and qualifying terms.

- Transfer your AVCs to another provider

If you transfer your AVCs to one or more different providers, each will offer different options for what you can do with them, including the option to buy an annuity. Each of the different options will have different features, rates of payment, charges and tax implications.

Should you talk to a financial advisor?

The Pension Helpline is not allowed to offer you financial advice. If you are unsure about how to manage your AVC investments, you should consider speaking to a financial advisor or get free and impartial guidance.